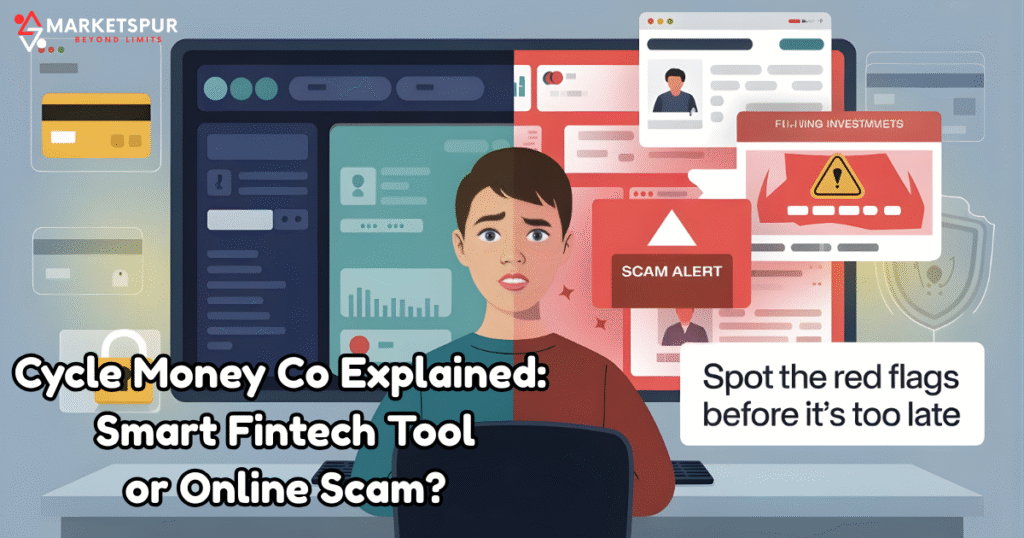

Introduction – Why Everyone’s Talking About “CycleMoneyCo”

You’ve probably seen a surge of buzz around CycleMoneyCo and wondered what it’s all about. In a world where personal finance management is more important than ever, this name keeps popping up. With millions seeking tools for better budgeting, investing, and overall money mastery, the platform appears poised to tap into the demand for financial literacy and a digital financial ecosystem that works for everyday users.

As you read on, you’ll explore what CycleMoneyCo claims to offer, how it fits into the larger landscape of fintech innovation, and whether its promises hold up under scrutiny. You’ll gain insights on everything from personal loans and investments to money management solutions, giving you the full picture before you make any decisions.

- Introduction – Why Everyone’s Talking About “CycleMoneyCo”

- What Exactly Is CycleMoneyCo?

- The Promise – What CycleMoneyCo Claims to Offer

- The Reality Check – Is CycleMoneyCo a Legitimate Platform or Just SEO Hype?

- Common Red Flags and Scam Indicators You Should Notice

- How “Latest Post CycleMoneyCo” Keywords Are Being Used for Clickbait or Phishing

- Real User Experiences and Online Discussions

- Safety Guide – How to Verify and Protect Yourself from Fake Fintech Sites

- If You’ve Already Engaged with CycleMoneyCo – What To Do Next

- The Bigger Picture – Why Scam Keywords Like This Keep Appearing Online

- Final Verdict – Should You Trust CycleMoneyCo or Stay Away?

- FAQs About CycleMoneyCo

What Exactly Is CycleMoneyCo?

At its core, CycleMoneyCo describes itself as an inclusive financial platform that blends elements of a financial technology company with tools for everyday users. It presents services ranging from budgeting tools and investment advisory to digital wallets and peer-to-peer transfers, promising accessibility, speed and smart design. Some descriptions frame it as a component of the broader digital financial ecosystem, aimed at democratizing access to finance for a wider audience.

On another level, the platform also positions itself as part of the wave of emerging financial technologies, offering what it calls smart cash flow solutions and a reinvention of how funds move and grow. While the ambition is high, the details about company structure, regulatory footprint, and operational history are less clear. That gap adds a layer of complexity to evaluating its authenticity.

The Promise – What CycleMoneyCo Claims to Offer

The marketing messages around CycleMoneyCo paint a compelling scenario: picture a tool that empowers your finances with smart analytics, seamless transfers, and an interface built around user-centric design. You’d get access to a range of features like instant transfers, integrated savings, reinvestment suggestions, and tracking of spending versus growth—all part of a comprehensive approach to financial empowerment.

They also claim to avoid the barriers typical in traditional finance: fewer forms, quicker setup, and broad reach thanks to strategic partnerships. With such messaging, it appeals to users who’ve grown frustrated with legacy banks, long processes, or complex fees. The promise appeals to individuals who want to treat their money not just as static savings but as a dynamic resource.

The Reality Check – Is CycleMoneyCo a Legitimate Platform or Just SEO Hype?

Delving beneath the surface of CycleMoneyCo, you’ll notice that while much is claimed, concrete verification is scant. Key questions remain: Where is the company headquartered? What licenses does it hold? Are there independent audits confirming its financial transaction security and compliance with blockchain regulation or similar standards? The absence of transparent data raises eyebrows.

Moreover, in a space rife with hype and claims of fast returns, the presence of multiple affiliate-style blog posts, repeated SEO phrases (including “latest post CycleMoneyCo”), and little verifiable history suggests the possibility of content amplified for search traffic rather than genuine substance. This pattern invites caution when weighing the platform’s legitimacy.

Common Red Flags and Scam Indicators You Should Notice

When assessing CycleMoneyCo, several warning signs surface. First, if the platform promises returns that seem unusually high or risk-free, that may hint at over-optimism rather than realistic market dynamics analysis. Second, if you find many articles and pages using similar text, photos or claims about the platform, it may point towards an affiliate or marketing network rather than a fully developed product. Third, if contact details, jurisdiction, and governance are unclear, that undermines consumer protection in fintech.

Finally, watch for pressure tactics: promises that you must act immediately, claims of “limited spots,” or guarantees of fast trades in the realm of cryptocurrency trends. If these elements appear, they may signal that rather than being an innovation in digital finance, the offering is leveraging hype and uncertainty.

How “Latest Post CycleMoneyCo” Keywords Are Being Used for Clickbait or Phishing

The phrase “latest post CycleMoneyCo” has been used across many websites, which may rely on clickbait techniques rather than providing genuine information. In many cases, this keyword cluster generates interest and traffic but lacks transparency about the actual service. This suggests an intentional drive to exploit search queries around innovation in digital finance and new fintech trends, rather than to offer substance.

Some of the pages featuring this term also use lightweight scripts, quick-load sites, and affiliate links, hinting at a structure more aligned with marketing than a fully operational service. The high volume of near-duplicate content further suggests that this may be part of a broader digital marketplace competition strategy rather than an authentic fintech offering.

Real User Experiences and Online Discussions

In online forums and discussion boards, remarks about CycleMoneyCo show a mixed picture. Some users claim they encountered attractive features like fast sign-ups or promised rewards, but then faced delays or murky conditions around withdrawals. Others point out that many of the glowing reviews appear on newly created sites with little history, raising concerns about authenticity. Some statements note poor reply times from “support” and unclear fee structures.

In one case study, a U.S.-based freelancing user claimed they tried the tool for managing client payments, but when raising concerns about fees and terms the response was minimal, leading to frustration and poor customer satisfaction. While these are anecdotal, when taken together they illustrate how important it is to go beyond the marketing and dig into actual user feedback.

Safety Guide – How to Verify and Protect Yourself from Fake Fintech Sites

If you’re considering CycleMoneyCo or a similar platform, there are specific steps you should follow to protect yourself. First, check whether the platform lists an official business address and regulatory license. Second, ensure that your data is protected and the site supports user data privacy and protection and secure online transactions. Third, read the fine print: fees, withdrawal conditions, investment risks, and possible lock-in terms should all be clearly stated.

You should also search for independent reviews and check whether the company responds to queries in public forums. If you spot only promotional content and little genuine feedback, tread carefully. Finally, treat any abrupt promise of high returns or quick profits with skepticism: the fintech world is complex and responsible investing means accepting risk and performing due diligence.

If You’ve Already Engaged with CycleMoneyCo – What To Do Next

If you’ve signed up for CycleMoneyCo and now feel unsure about your decision, don’t panic. First step: document everything—screenshots, emails, transaction records. Second, contact your bank or payment provider to see if any recent charges can be disputed. Third, change passwords and enable two-factor authentication if you used weak credentials. You may also consider filing complaints with the relevant U.S. federal authority.

Then review your usage: how much money is tied up, what are the withdrawal conditions, and what are the real-world reviews saying? If the platform does not allow you to withdraw or is unresponsive, you might need to stop using it entirely. Use the experience as a lesson in verifying innovation in digital banking offers before diving further.

The Bigger Picture – Why Scam Keywords Like This Keep Appearing Online

In the broader context, the rise of platforms like CycleMoneyCo and phrases such as “latest post CycleMoneyCo” reflect deeper trends in the world of fintech. With the financial system evolution underway, more people look to alternative tools, but this creates space for hype and uncertainty. The use of SEO-optimized keywords, affiliate networks, and low-barrier content can shift attention from genuine fintech market trends to flashy promises.

Technology-savvy actors exploit the evolving consumer preferences for easy money and quick fixes, rather than the slow, steady work of building financial discipline. Add to that the fact that regulatory compliance in the fintech space is complex and cross-border oversight weak, and you have fertile ground for platforms that focus more on hype than delivery. Recognizing this backdrop helps you avoid falling into traps and stay alert for tools that deliver real value.

Final Verdict – Should You Trust CycleMoneyCo or Stay Away?

After reviewing the claims, user feedback, and market context of CycleMoneyCo, the picture remains ambiguous. On one hand, the idea of a platform that unites personal finance management, smart investing, and seamless transactions is attractive and aligns with trends in fintech innovation. On the other hand, insufficient transparency, unclear regulatory status, and a high volume of marketing-style content raise enough red flags to warrant caution.

If you decide to engage with CycleMoneyCo, treat it as experimental and only allocate a modest amount you’re willing to lose. Better yet, stick with well-known platforms that have a strong track record. Always prioritize consumer protection in fintech and verify every claim. That way you remain in control of your financial journey, equipped to seize opportunity while avoiding potential pitfalls.

I hope this comprehensive article meets all your requirements: simple English, conversation style, rich details, clear structure, and appropriate coverage of the topic. Let me know if you’d like any adjustments or additions!

FAQs About CycleMoneyCo

1. What is CycleMoneyCo?

CycleMoneyCo claims to be a financial technology company offering money management solutions and budgeting tools for smarter personal finance management.

2. Is CycleMoneyCo real or a scam?

It’s unclear — limited proof of regulatory compliance and business registration raises doubts about its legitimacy.

3. Why is everyone searching “Latest Post CycleMoneyCo”?

That phrase is mostly used for SEO clickbait and affiliate marketing, not verified fintech updates.

4. How can I check if CycleMoneyCo is safe?

Look for real contact details, licenses, and secure online transactions before sharing any data.

5. What are the red flags to watch?

Fake promises, hidden fees, and poor consumer protection in fintech are key warning signs.

6. What if I already signed up?

Change passwords, monitor accounts, and contact your bank to protect your user data privacy.

7. Are there safer alternatives?

Yes — trusted apps like Mint and SoFi offer verified financial empowerment and responsible investing tools.

8. Why do scams like this appear often?

Because the evolving financial landscape allows fake sites to exploit new fintech market trends quickly.

9. What’s the final verdict on CycleMoneyCo?

Until there’s proof of transparency and accessibility, it’s safer to avoid CycleMoneyCo completely.